The journal: education

NQ Futures Risk Management: How to Size Positions

NQ is a high-leverage instrument. A single contract moves $20 per point — and NQ regularly moves 50–100+ points in a session. That's $1,000–$2,000 per contract, per session, in either direction.

Position sizing isn't a nice-to-have on NQ. It's the difference between a losing week and a losing account.

The Foundation: Risk Per Trade

The starting point for any NQ risk framework is defining a fixed dollar amount you're willing to lose on a single trade. This is your risk per trade.

Common approaches:

- Fixed dollar amount (e.g., $200 per trade regardless of setup)

- Percentage of account (e.g., 1% of account per trade)

For most traders, 1% of account per trade is a reasonable starting point. At 1%, you can take 10 consecutive losses before being down 10% — a realistic worst-case drawdown to plan for.

Example:

- Account size: $25,000

- Risk per trade (1%): $250

- Each full point of NQ = $20

If your stop loss is 12.5 points from entry, then:

Max contracts = Risk per trade ÷ (Stop points × $20 per point)

Max contracts = $250 ÷ (12.5 × $20) = $250 ÷ $250 = 1 contract

At 2 contracts with the same stop, you'd be risking $500 (2% of account). Sizing up is a choice you make consciously with this math, not by feel.

The Role of the Stop Loss

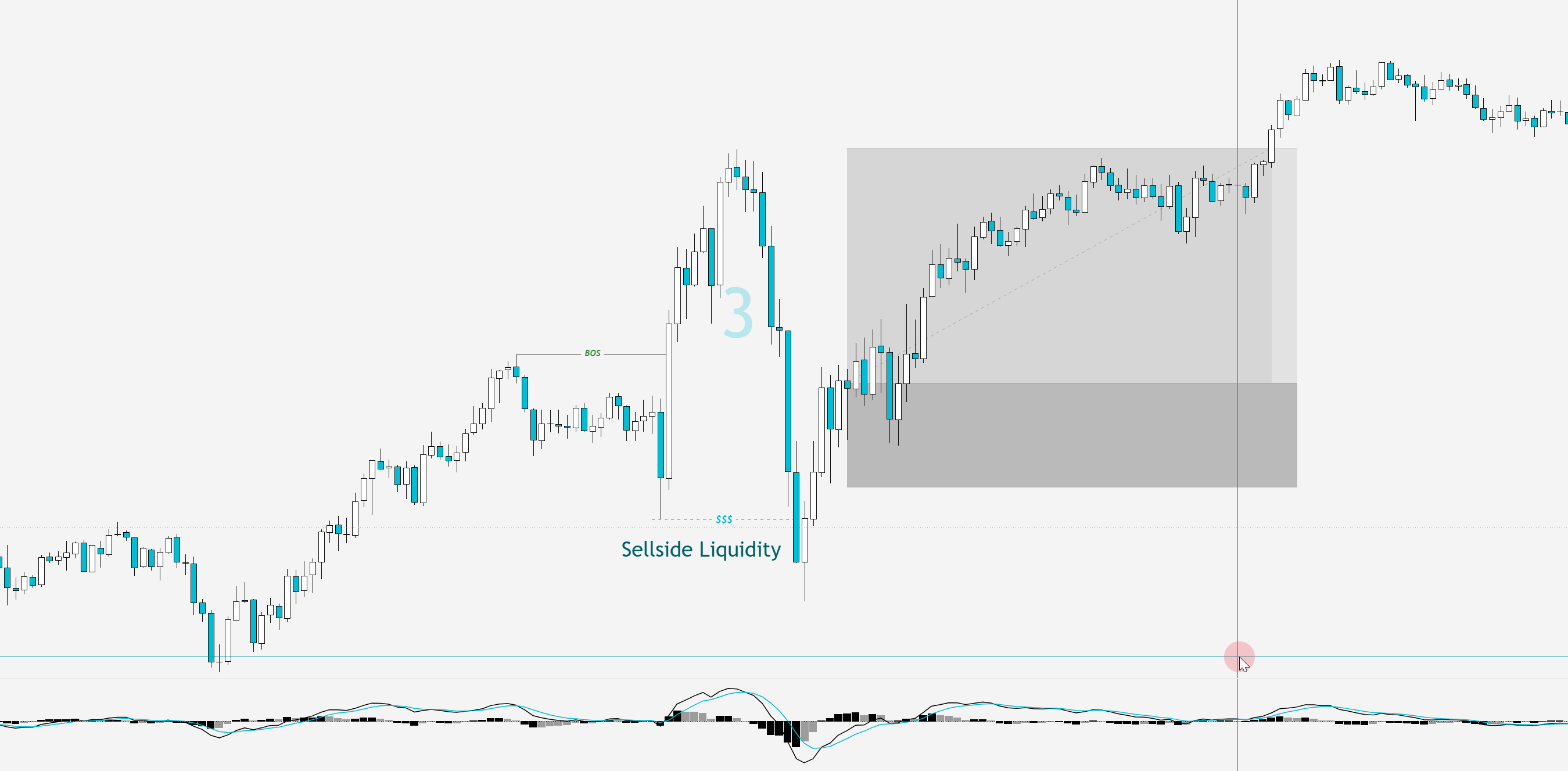

In the LS Model, the stop loss is defined by the setup — not chosen arbitrarily after the fact. Every entry fires off a 3m trigger, and the stop sits at the developing 3m structure that produced it:

- Long setup: SL below the developing 3m structure

- Short setup: SL above the developing 3m structure

That structure is the invalidation point. If price breaks back through the structure that confirmed the entry, the trade thesis is wrong. Anchoring the SL to structure keeps it at a logical, market-driven level rather than a round number or gut-feel distance.

The implication for sizing: Your stop distance changes trade by trade, depending on the structure of each setup. Position size should adjust accordingly — not the stop.

A wide SL means fewer contracts. A tight SL allows more contracts. The dollar risk stays constant; the size floats.

Breakeven at 1:1, Single Exit at Liquidity

The LS Model's management is deliberately simple:

| Step | What Happens | |------|--------------| | At 1:1 | Stop moves to breakeven — the trade can no longer lose | | After breakeven | Stop trails the developing 3m structure | | At the liquidity target | Position closes in full — one exit, no partials |

The target itself is the next opposing pool of liquidity, and risk-to-reward is a floor for taking the trade at all: 1:2 minimum on a Continuation (ideally 1:3), 1:2 cap on a Bias Flip, 1:1 on an Opening Drive. Why there's no TP1/TP2 ladder is covered in Why the LS Model Exits Once.

The session rules: Max 2 trades per NY session, and stop trading for the day after 2 losses. This discipline prevents chasing.

The Micro E-Mini: Learning Without Full NQ Exposure

For traders building toward NQ, the Micro E-mini (MNQ) offers the same market at 1/10th the contract size: $2 per point instead of $20.

The same methodology applies. The same setups fire. The same stop loss levels are valid. The only difference is scale.

At MNQ sizing, a 12.5-point stop loss costs $25 per contract instead of $250. This makes MNQ appropriate for:

- Traders with smaller accounts (under $10,000)

- Traders learning the methodology before scaling

- Testing a new approach without full NQ exposure

The risk per trade math is identical — just substitute $2 per point. A $100 risk budget with a 12.5-point SL on MNQ = 4 contracts. The same position in NQ would cost $250 for 1 contract.

What Not to Do

Don't use fixed contract size without accounting for SL distance. Taking 1 contract on every trade regardless of stop width means your dollar risk varies wildly between trades. A 5-point SL costs $100 per NQ contract; a 20-point SL costs $400. Same position, very different risk.

Don't move your stop loss to avoid a loss. If price is approaching your SL, that's the setup working as designed. Moving the stop widens your risk exposure in real-time and turns a defined-risk trade into an undefined one.

Don't size up to "make back" a loss. After a losing trade, the temptation to increase size on the next setup to recover quickly is strong. It's also the fastest path to compounding losses. The next trade should be sized identically to the previous one — risk stays constant, not outcome-dependent.

Don't count on the full target every trade. Some trades go to breakeven and the trail takes them out early. Position sizing should be built on a realistic outcome distribution, not "every trade reaches the liquidity." The breakeven move at 1:1 is what keeps those partial moves from costing you.

A Simple Sizing Workflow

Before entering any LS Model setup:

- Get the SL level from the setup's structure: beyond the developing 3m structure that confirmed the entry

- Calculate stop distance: Entry price − SL price (in points)

- Multiply by contract value: Stop points × $20 (NQ) or × $2 (MNQ)

- Divide your risk budget by that number: Risk per trade ÷ (stop points × point value) = contracts

- Round down to the nearest whole contract

If the math produces fewer contracts than you want to trade, the correct response is to accept the sizing — not to widen your stop.

The Long View

NQ risk management isn't about any single trade. It's about surviving long enough to let the methodology play out over a large sample of trades.

A strategy with a 55% win rate and 1.5R average winner needs dozens of trades for that edge to manifest consistently. Overleveraging or abandoning the sizing rules after a few losses means you might not be in the game long enough to see the edge work.

The two-trade session limit, the defined stop loss on every setup, and the single-exit management are built for longevity. They exist because a single bad day shouldn't threaten the account.

Trading futures involves substantial risk of loss and is not appropriate for all investors. This content is educational only and does not constitute financial advice. Past results do not guarantee future performance.

Related reading: Stop Loss Placement on NQ Futures covers the logic behind where SLs go. Why the LS Model Exits Once explains the management from entry to close. Or join the free Discord to hear the levels called live.

Get the weekly NQ Edge letter, free.

Want to sit in the room?

Trade NQ live with me every NY open.

Pre-market read, the entry called as price gets there, full debrief after. You watch the read, not just the result.